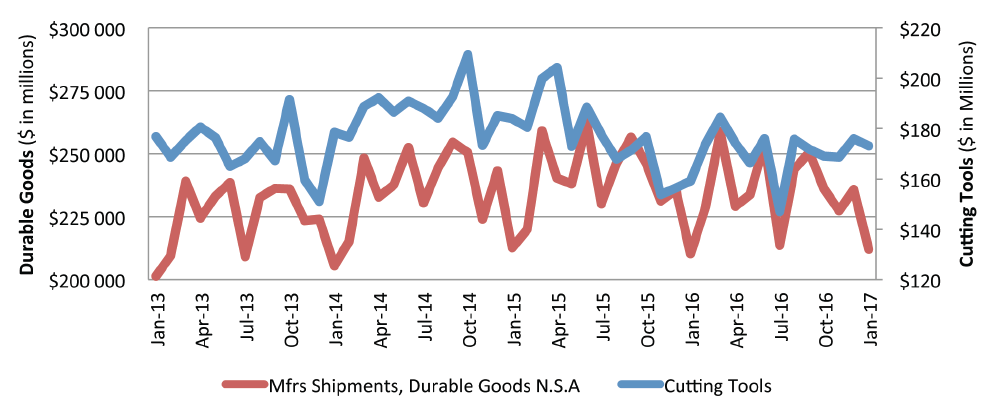

January U.S. cutting tool consumption totalled $173.05 million according to the U.S. Cutting Tool Institute (USCTI) and AMT – The Association For Manufacturing Technology. This total, as reported by companies participating in the Cutting Tool Market Report (CTMR) collaboration, was up 8.7% from December’s $159.17 million and up 8.7% when compared with the total of $159.22 million reported for January 2016. With a year-to-date total of $173.05 million, 2017 is up 8.7% when compared with 2016.

These numbers and all data in this report are based on the totals reported by companies participating in the CTMR program. The totals represent the majority of the U.S. market for cutting tools.

Brad Lawton, Chairman of AMT’s Cutting Tool Product Group states that, “the early numbers for the first month of 2017 support the optimistic feelings that are growing in the domestic manufacturing market. For the export of U.S. made cutting tools it is hoped that the strength of the U.S. Dollar and the Trump Administration trade policies will not destroy this potential business. We must all wait and see the numbers at the end of the first quarter.”

“The latest data indicate cutting tool shipments are on a somewhat firmer footing in early 2017. The overall trend in durable goods orders and shipments points to firming activity after a lacklustre 2016 performance. Likewise, most leading manufacturing indicators show improving domestic and global confidence levels,” says Gregory Daco, Chief U.S. Economist at Oxford Economics. “President Trump’s pro-growth fiscal agenda should stimulate activity by year-end and into 2018, though his protectionist and anti-immigration agenda represent notable downside risks.”

Airbus welcomes the signature of a new chapter of the Memorandum of Cooperation (MoC) in Civil Aeronautical Industry between the Ministry of Economy, Trade, and Industry of Japan (METI) and the Directorate General for Civil Aviation of the Ministry of Ecology, Sustainable Development and Energy (MEDDE) of the French Republic.

The agreement was signed in Tokyo between Toshihide Kasutani, Director-General, Manufacturing Industries Bureau of METI, and Thierry Dana, French Ambassador to Japan.

With this agreement, which aims to strengthen the cooperation between Airbus and the Japanese industry, an Airbus-Japan Ad Hoc Civil Aeronautical Industry Working Group will be established, and it will meet on a regular basis to discuss technology fields that could be considered for cooperation between Airbus and Japan such as material, aircraft system and equipment, or manufacturing technologies for the development of future Airbus aircraft.

“We are very pleased that Japan and France are together providing support for enhancing our partnerships between Japan and Europe,” said Stéphane Ginoux, President of Airbus Japan. “We see Japan as a key country for partnerships in areas such as future aircraft technologies, R&T and digital innovation. We are committed to expand our industrial footprint in Japan further.”

The European machine tool industry was represented by Galdabini, President of CECIMO and Managing Director of Galdabini SPA in the European Industry Day. As debater in the high-level panel on SME access to technologies, Galdabini highlighted that cross-border collaboration between machine tool builders and technology centres is essential, but severe bottlenecks, hampering the competitiveness of industry, exist.

Mr Luigi Galdabini, President of CECIMO and Managing Director of Galdabini SPA.

“If European machine tool builders want to keep up with market trends, they need to be increasingly agile, develop new solutions that match the changing needs of machine tool users, and focus on incremental innovation, offering continuously improved goods and services to customers. Consequently, technology centres spread across Europe can join forces with manufacturing SMEs and help them in responding to these evolving demands. At strategic level, MT builders need more policy instruments that foster the link between research and business, and they also call for incentives, which underpin cross-border collaboration in Europe and support the internationalization of manufacturing SMEs” added Galdabini.

Mr Filip Geerts, CECIMO Director General.

CECIMO and 124 European manufacturing associations recently launched a Joint- Declaration that calls the European Commission, the European Parliament and the Competitiveness Council to define and implement an ambitious and coordinated European industrial strategy. “CECIMO finds it very positive that the European Commission organized the first European Industry Day. Nevertheless, to safeguard the world leadership of European manufacturers and jobs in Europe, the Commission needs to follow up what stakeholders have been voicing and to come up with a comprehensive action plan focusing on the strengths of our businesses” stated Mr Filip Geerts, CECIMO Director General.

The Joint-Declaration for an ambitious EU industrial strategy highlights that, while competitors from across the world put industry at the very top of their political agendas, develop and implement well-thought strategies, the EU falls behind its industrial policy targets. “There has been no better time to reaffirm Europe’s commitment to manufacturing, innovation and jobs. European associations representing 125 manufacturing sectors are ready to offer their cooperation to the European Institutions” points out Geerts.

Standards on the safety of machine tools are currently being revised by the VDW (German Machine Tool Builder Association). The VDW’s working group for Safety engineering in metal-cutting machining is especially tasked with the Type C Product Safety Standards coming first in terms of importance, e.g. ISO 16089 for grinding machines, ISO 16090 for milling machines and ISO 23125 for lathes.

They all refer to the Type-B Standard ISO 13849-1, in which what are called safety functions are given probability-referenced ratings as models for control chains. This theoretical approach intermeshes with operationally validated practice already established in the field. Despite a demonstrably high level of safety in German machine tools, however, further clarification is still needed, since the importance of safety functions is not yet perceived from a harmonized viewpoint in the above-mentioned standards, because there are technology-specific differences in interpretation. The recently expanded company participation in the VDW’s working group has increased the need for clarification still further, since besides metal-cutting processes, presses and lasering machines were also included last year. The latter have no normative stipulations at all for safety functions.

Insurers take a stance on operating modes

Another controversial issue is a machine’s operating modes, e.g. when the machining process has to be set up and meticulously observed in operation. Trouble-shooting and maintenance can be particularly problematic in this context, if safety features are deactivated for the purpose: in the case of the Golden Tongue (as a manipulatively feigned signal erroneously communicating that Guard doors are closed and locked), the accident risk, according to surveys conducted by the DGUV (German Statutory Accident Insurance Agency) is approximately 10 to 20 times higher than in undisturbed production operations. Now, in January 2017, following nationwide consultation, the DGUV announced a position paper that so far is manifestly aimed only at machinery manufacturers. It is entitled: Instructions for manufacturers on risk assessment of machines and machinery systems with reference to the aspect of measures to counteract manipulation of safety features.

Because the manipulation of safety features, however, is closely connected with operational framework conditions, involvement of the VDW is essential, so that the DGUV’s paper takes a holistic approach. The intention is to present a harmonized standard on the VDW’s Safety Day at EMO Hannover on 19 September 2017.

The “Golden Tongue” is passé

To quote Peter Steger, Head of Electrical Design at Grob-Werke in Mindelheim, “It’s the end of the line for the “Golden Tongue”, a multi-purpose key for manipulating protective features. It enabled staff operators to make the control system erroneously believe that the guard door is closed and locked.” Photo: Grob

Interview with Peter Steger, Grob-Werke, Mindelheim, Germany

In this interview with Peter Steger, a design engineer at the Grob company in Mindelheim and a member of this VDW working group, it clearly emerges how meticulously critical interactions between man and machine have to be tackled in order to master the increased risk involved. In this context, the above-mentioned Type C standards give the design engineers argumentative backing with operating modes defined in general terms (such as Service Mode) that are also regularly addressed in the working group itself. In addition, some firms are adopting their own individualized approaches, in order to avoid the universally deplored manipulation with manufacturer-specific operating modes; this means certain maintenance activities at the machine are carried out only by the company’s own service personnel.

Steger from Grob-Werke in Mindelheim explains how manufacturers are supporting users of their machines in their thrust for more occupational safety.

Peter Steger, Grob is acknowledged as a model company when it comes to occupational safety: how do you handle this issue internally with your own machine operators?

PS: For working safely with machine tools, it’s vital that the employees concerned are adequately briefed about the dangers involved in working with machine tools and about the protective measures for averting them. Apart from the operator training courses themselves, our operators accordingly receive regular briefings on the subject of health and safety.

Besides general instructions on safety-compliant behaviour, the insights gained from the relevant risk assessment of the workplace involved and the equipment used there are incorporated. In this case, for example, the hazard-related factors when working with machine tools and the protective measures that have to be complied with. The protection concept for our operators is rounded off by additional information on site (such as an operating manual for safety-compliant working with the machine tool).

And what about the instructors for the operators?

PS: We additionally send our forepersons to external seminars held by the Employers’ Liability Insurance Association, to raise their awareness of their managerial duties and remits – not least in regard to occupational safety. I am delighted to note that above all our new young forepersons are being trained by outside lecturers, and are thus learning even more about the important role played by the duty of care for employees The experience they gain in these outside seminars helps the forepersons, since they can utilise the tips in actual practice to optimum effect.

So it’s also a tip that customers should take on board?

PS: Definitely. What’s important for our people counts just as much for our customers.

And how does Grob train its customers?

PS: When we sell extensive production lines, we offer our customers training courses specifically tailored to the requirements of the customer concerned. For multi-purpose machines, we have a range of complementary training modules: these include for example, process-compliant programming, helical interpolation and geometrical calibration. We also, of course, always talk about how to handle the machines safely and provide examples from actual practice.

Could you cite a typical example for us?

PS: When our customers are already working with one of our machining centres, we show them ways and options for increasing their productivity. Thanks to our training courses, they become even more familiarized with our machines and learn how to operate them safely. New customers, too, benefit from our training courses, which contribute towards proactive safety and demonstrate efficient working practices. Various measures are presented for reducing the stress on machines and tools, shortening the make-ready times and ensuring full capacity utilization at the machine. This in its turn contributes towards upgrading quality levels. Working with machine tools, after all, stands and falls with the quality of the control system.

How can it contribute towards occupational safety?

PS: As far as I’m concerned, this primarily includes malfunction and error messages on the consoles of the machines’ control systems, which tell the operators the reasons for a machine standstill, for example.

How else do you support users in terms of occupational safety?

PS: We make sure that no hazards can be created by the machine when separating safety guards are opened, and that it can be operated without manipulating any protective features.

This applies primarily to make-ready mode: what regulations have to be complied with in this situation so typical for production operations?

PS: The important ones are Operating 2 and 3 as EN 12417, plus in the future MSO 2 and 3 in accordance with FDIS ISO 16090 Safety of Milling Machines. MSO stands for Mode of Safe Operation and FDIS for Final Draft International Standard. In these safe operating modes, the staff can safely operate a machine in very many functions even when the door is open, using a portable device. They can try out movements in the machine, for instance, without manipulating the production line in any way.

How do you proceed in your own production operations?

PS: For our own highly qualified personnel, we have internally defined the Grob operating mode, which goes beyond the functions of the normative operating modes MSO 2 and 3 that I’ve already mentioned. These operating modes restrict operations by imposing limits, regarding the speed, for example. For everyday work in test runs, however, these limits are not very helpful. With the Grob operating mode, you can overcome these limits without manipulating the machine.

So you’re offering safety without any loss in speed, meaning without any impairment of productivity: wouldn’t this function be of interest to customers as well?

PS: For them, there are already the normative operating modes MSO 2 and 3 that I’ve already mentioned. We do, of course, get asked, to enable the Grob operating mode for customers’ maintenance staff as well. But given the ongoing standards situation, this is not permissible without appropriate measures and processes to be put in place by the customer concerned.

What do you think about the use of electronic safety switches of Type 4 as defined in ISO 14119 “Safety of interlocking devices”, which protect the machine against manipulation using radio technology, for example – keyword RFID?

PS: Without a doubt, there is an interesting new trend towards highly encoded safety switches designed to preclude the possibility of manipulation. This signifies the end of the line for the Golden Tongue, a multi-purpose key for manipulating protective features. You see, it enabled staff operators to make the control system erroneously believe that the guard door is closed and locked.

What topics can visitors to the Grob stand at EMO Hannover 2017 learn more about in terms of occupational safety?

PS: Visitors to our stand at EMO Hannover 2017 will learn more about occupational safety, ergonomics and the relevant courses available. Our customer training team will be there on the spot and presenting courses designed to provide our customers with valuable tips on how to handle our machines.”

Peter Steger, thank you for talking to us.

The interview was conducted by Nikolaus Fecht, specialist journalist from Gelsenkirchen.

It would be the ideal Who-Wants-to-be-a Millionaire quiz question: where do machinery manufacturers, architects, construction engineers and electrical engineers all work together under the same roof? The answer is: in the ETA factory of Darmstadt University of Applied Science. Together with private companies, it is tackling a keynote topic of EMO Hannover 2017, the world’s premier trade fair for the metalworking sector, live and in colour. How can machine tools’ appetite for energy be downsized in interactive coordination with all systems, and how can firms actually put this expertise into practice?

To quote Prof. Dr.-Ing. Eberhard Abele, Director of the Institute for Production Management, Technology and Machine Tools (PTW), at Darmstadt University of Applied Science, “in conjunction with machinery manufacturers, construction engineers and architects, we are aiming to analyze and optimize on a cross-disciplinary basis machine components, production machines, the process chain, a building’s technical equipment and its envelope and envelope from the viewpoint of energyefficiency.” Photo: Press Agency Fecht

In Hanover, the first specific solutions for the energy-efficient production operations of tomorrow will be unveiled, not least by Bosch Rexroth. The company is working closely together with the researchers in Darmstadt.

Professor Eberhard Abele, Director of the Institute for Production Management, Technology and Machine Tools at Darmstadt University of Applied Science, saw his heart’s desire granted in 2000. The cybernetics graduate, with a doctorate in mechanical engineering, was born in Waldstetten (Schwäbisch Gmünd County), and after 15 years in the industrial sector wanted to build a factory at the University of Applied Science, so as to educate students under realistic conditions. Professor Abele has meanwhile even seen his wish come true twice – in 2007, the bustling Swabian founded the Process Learning Factory (CiP) in Darmstadt, and in 2016 the Energy-Efficiency, Technology and Application Centre (ETA factory).

Training and researching energy-efficiency

His motivation was self-evident to him – while CiP serves as a competence centre for lean production and Industry 4.0, the ETA factory was tasked with training and research in the field of energy-efficiency. It is required, for instance, to serve as a learning factory, with whose aid Darmstadt University of Applied Science also aims to integrate the topic of energy-efficiency into the curricula for mechanical and construction engineers. To quote Professor Abele, “today, all first-semester mechanical engineering students are already being confronted with the potential for energy savings in production operations. In subsequent semesters, they then find an almost ideal environment for trying out their own creative approaches to improved energy-efficiency in dissertations and theses.”

The ETA factory, however, is primarily – as a large-scale research laboratory for industrial energy-efficiency, helping the German government to halve energy consumption by 2050 in comparison to 2008. In this context, the industrial sector plays a crucial role, since according to the German Federal Environmental Agency it consumes nearly a third of the total energy in Germany. Reason enough for the nation’s Federal Ministry of Economic Affairs and Energy (BMWi) to subsidise the ETA factory’s construction, its entire equipment and its long years of research work with 15 million euros.

Improving the interaction of all components

It is tasked with holistically improving the coordinated interaction of all a factory’s components and systems – from the machine tools to the building’s technical equipment and envelope, so as to downsize its overall energy consumption. On the same area as a typical indoor handball court (around 800 square metres), there is not only a learning area for students and employees from the industrial sector, but also a machinery zone with machine tools and cleaning machines plus a hardening furnace – an environment in which components for pumps (to be precise: control disks for hydraulic axial piston pumps) are produced: the ETA factory covers all stages of industrial manufacture, from the blank to the finished part.

Large-scale research laboratory for industrial energy-efficiency – the ETA-factory supports the ambitious goal of halving the energy consumption in Germany by 2050 compared to 2008. Photo: PTW

The production of pump components, however, is only a means to an end, since it’s here that new concepts for energy savings are being developed under real-life conditions. The former state of the art has been that individual components are scrutinised separately, says Institute Director Professor Abele. “In conjunction with machinery manufacturers, construction engineers and architects, we are aiming to analyse and optimise on a cross-disciplinary basis machine components, production machines, the process chain, a building’s technical equipment and its envelope from the viewpoint of energy-efficiency.”

Besides design-enhancing production processes, other focuses include the coordinated interaction between the technical equipment and the machinery. The technical leitmotif here is multiple networking of the factory’s individual modules – a heat network links the machines together and to the building’s envelope using heat pipes. The façade incorporates an integrated array of very small tubes, enabling it to react to the temperatures outside, and respond accordingly, either by cooling or heating the water in the pipes. It is supported in heating the factory hall through the heat networks by the waste heat from the machines, though this is also utilized by other systems, like the hardening furnace. “Customarily, the water used for cooling the machine’s drive elements is continuously cooled down again,” says Abele. “This is simply a total waste of energy. We now no longer cool down the entire water supply, we even heat it up a bit to 80 degrees Celsius – for the downstream system that cleans the metal parts, to cite one example.” For cooling the drive elements, the machines instead use cold water from the mains.

The ETA factory also possesses a data network that links together all the areas involved, “We combine the control of energy consumption with Industry 4.0,” emphasises Abele. “In this way, the acquired and edited data, meaning big data, can be used for optimizing the energy consumption.”

The ETA factory is an international role model

But it’s not just in Germany that the new form of downsizing energy consumption with the aid of a research factory is arousing keen interest. For instance, business engineer Martin Beck, Group Leader for Eco-Compatible Production at the ETA factory, is advising a company that’s setting up an energy-efficient machine factory in Singapore. But the expert has encouraging words for small and mid-tier companies too, urging them to take advice from the ETA factory or from other existing energy-efficient factories.

To quote Hansjörg Sannwald, Head of Sectoral Management Machine Tools at, Bosch Rexroth AG, Lohr am Main, “the software will know in advance the machines’ upcoming consumption values, and will be able to shift load peaks against each other. This, however, is absolutely conditional upon open communication standards and decentralized intelligence.” Photo: Bosch Rexroth

“It pays off for mid-tier enterprises, in particular, who won’t usually possess an energy efficiency department of their own,” says Beck. “The energy costs account for around 3 to 5 percent of the total costs, of which we can save 10 to as much as 40 percent using rigorously targeted, holistic, often state-subsidized consultancy.” The expenditure on what are called energy-intensive industries in Germany, says their Bonn-based umbrella association (EID), are particularly high: every year, they spend more than 5 percent of their turnover (around 17 billion euros) on energy.

In addition, the ETA factory (says a PTW newsletter) serves as a large-scale research device for ambitious projects. These include the Copernicus project entitled SynErgie – Synchronized and energy-adaptive production technology for flexible matching of industrial processes to a fluctuating energy supply currently being subsided by the government with 30 million euros. There are about 100 partners involved in this project, from the industrial sector, the research community and society as a whole (e.g. the trade union IG Metall, Friends of the Earth Germany (Bund Naturschutz BN)). Project Director Abele, who is also President of the German Academic Society for Production Engineering (WGP) defines the goal as follows, “we are networking wind turbines and solar modules with the production machine.” Alternative energies like wind and solar power mostly produce either too little or too much energy.

“We want to render the production facilities so flexible that they can themselves react to this fluctuating supply of energy,” says PTW Senior Engineer Stefan Seifermann. This is an important undertaking, since renewable energies in Germany were already accounting for 31 percent of the gross power consumption in 2015.

Metal-cutting research – besides a learning area for students and employees from the industrial sector, the ETA factory possesses an authentic production line for pump components. Photo: PTW

SynErgie is initially beginning with seven energy-intensive sectors, one of which is machinery and plant construction. The connected load of the individual pieces of equipment concerned is in this sector significantly lower, but conversely very many more machines and lines are used than in other branches of industry. There is keen interest from this sector, as a glance at the participants shows: under the leadership of Professor Matthias Putz from the Fraunhofer IWU in Chemnitz, firms like Bosch, Festo, Handtmann, Hirschvogel Automotive, Siemens and Volkswagen Saxony are working together on this project.

The means to the coordinatory end are highly dynamic control platforms that take due account of the fluctuating energy supply, and regulate accordingly the energy distribution between industrial processes like cleaning, hardening or metalworking. To quote Professor Abele: “Only when companies know when a lot or very little power is being generated from renewable energies, and the stock market is signalling this by low electricity prices, can they react appropriately.”

Bosch Rexroth: distributed intelligence and open interfaces Versus fluctuating power availability

Bosch Rexroth AG from Lohr am Main is participating in the SynErgie research project in order to develop open- and closed-loop control strategies designed to match the energy consumption to the fluctuating supply. For this purpose, the research project is prioritising distributed intelligence in the actuators and cross-manufacturer interfaces capable of also supporting Industry 4.0 applications.

Decentralized, intelligent control systems and drives from Bosch Rexroth will according to the company be capable in future of scheduling breaks to match the supply situation, and without any superfluous waiting time restoring readiness for production at the right juncture. This necessitates intelligent shutdown and ramp-up capabilities for the lines concerned. Rexroth will in future be equipping the drives, drive controllers and control systems with the appropriate software functions and cross-manufacturer interfaces. These interfaces support the requirements of Industry 4.0 concepts, and supplement them with a dimension of energy-efficiency.

Bosch Rexroth is also involved as a co-initiator of the ETA factory. Here, for example, under real-life situational conditions, researchers are addressing the process chain of a hydraulic component from the Rexroth plant in Elchingen, and communicating how energy can be utilized even more efficiently by using a new holistic approach and intelligent networking of the building envelope, the technical building equipment, the energy storage units and the production lines themselves.

To quote PTW Senior Engineer Stefan Seifermann, “We want to render the production facilities so flexible that they can themselves react to this fluctuating supply of energy.” Photo: PTW

Anyone interested can find out more details at EMO Hannover 2017, where Bosch Rexroth will be addressing not only the topics of networked hydraulics and Industry 4.0, but energy-efficiency as well. “Rexroth’s systematized 4EE concept (for Energy Efficiency) taps into cross-technology savings potentials in metal-cutting and forming production operations,” explains Hansjörg Sannwald, Head of Sectoral Management Machine Tools. For example, variable-speed pump drives for hydraulic systems consume up to 80 percent less power than their constant-speed counterparts.

But where do we go from here in terms of energy-efficiency? The expert is confident that networking based on Industry 4.0 will make it possible to couple all consumers in a production line or factory for optimized energy management. His vision, “the software will know in advance the machines’ upcoming consumption values, and will be able to shift load peaks against each other. This, however, is absolutely conditional upon open communication standards and decentralised intelligence.”

Industry domestic sales ended 2016 on a weak note with aggregate industry new vehicle sales for December, 2016 at 41 639 units recording a decline of 7 519 vehicles or a fall of 15.3% compared to the total new vehicle sales of 49 158 units during the corresponding month of December, 2015. The December, 2016 new passenger car market and light commercial vehicle market reflected a year on year volume change of -14.0% in the case of cars and -17.8% in the case of light commercial vehicles. Sales of medium and heavy commercial vehicles declined by 18.2% year on year.

In contrast, export sales had recorded an improvement in December, 2016 and at 18 668 units reflected a gain of 1 222 vehicles or 7.0% compared to the 17 446 vehicles exported during December, 2015.

Another challenging year with lower domestic sales offset by continued growth in vehicle exports

For the third year in succession, new vehicle sales during 2016 in South Africa recorded a year on year decline. The slowdown in the domestic economy, above average new vehicle inflationary pressures, increases in interest rates, pressure on consumers’ and household disposable income and low levels of consumer confidence had contributed to a double digit decline in annual domestic sales volumes. In the event, aggregate sales during 2016 fell by 11.4% in volume terms to 547 442 units compared to the sales total of 617 648 in 2015.

Overall, 2016 turned out to be another extremely difficult year for the South African automotive industry with domestic new vehicle sales progressively under pressure, particularly at dealer level, despite attractive sales incentives and a strong contribution by the car rental sector which accounted for an estimated 16.3% of new car sales during the year. Industry trading conditions had remained intensely competitive characterized by pressure on dealer margins. Preliminary estimates of 2016 motor industry new vehicle related sales turnover indicated a decline of about 2.0%, taking account of sales volumes, changes in mix and a weighted average estimated increase of about 14.0% in new vehicle prices – to reach about R233 billion for the year. Industry new vehicle export sales were estimated to have added a further R105 billion to total Industry 2016 revenue.

2016 Vehicle exports represented the highest annual Industry export figure on record and total vehicle exports at 344 822 units were up on the 333 847 vehicles exported in 2015.

Assuming further improvement in the global economy – industry export sales during 2017 could improve by some 30 000 vehicles or about 10.0% to reach a conservative projection of 375 000 export units.

In summary, the decline in domestic sales was offset to a limited extent by continued growth in vehicle exports which in turn assisted in sustaining utilization capacities and employment levels of vehicle manufacturers.

Industry prospects for 2017

Modest improvement in domestic new vehicle sales during the second half of the year together with further relatively strong growth in vehicle exports

2017 is expected to be another difficult year for the domestic SA auto industry, however, a modest improvement in new vehicle sales is expected during the second half of 2017.

Annual aggregate annual industry sales by sector, since 2010, were as follows –

[wpsm_comparison_table id=”4″ class=””]

Source: Lightstone Auto, NAAMSA

2016 Industry export sales data, compared to previous six years, were as follows –

[wpsm_comparison_table id=”5″ class=””]

Source: Lightstone Auto, NAAMSA

The outlook for 2017 in terms of Industry domestic vehicle sales by sector is summarised hereunder –

[wpsm_comparison_table id=”6″ class=””]

Industry production levels, on the back of expected further growth in vehicle exports, should however remain in an upward phase.

At this juncture, 2017 projections for South Africa reflect an expected improvement in GDP growth to around 1.5% (from 0.4% in 2016), in gross domestic expenditure to over 2.0% (from -0.3% in 2016), in growth in private consumption expenditure to about 2.0% (from 0.8% in 2016) and in fixed investment to around 2.2% (from -2.5% in 2016). Improvement in growth prospects is premised on the easing in drought conditions, the improvement in commodity prices, a decline in inflationary pressures on the back of a stronger Rand as well as recent improvements in the Purchasing Managers’ indexes and the Reserve Bank’s leading indicator. On the negative side, domestically, elevated political tensions are likely to continue to weigh on business confidence and the expected increase in taxes in this years’ budget will erode real purchasing power.

Internationally, volatile and uncertain conditions are likely to prevail during 2017. Elevated geo-political tensions and political uncertainty in major advanced economies associated with elections could heighten global risk aversion and trigger confidence shocks. Despite these considerations, the global economic outlook at this stage, remains positive and should continue to lend support to South Africa’s improving vehicle export performance. Ultimately, industry vehicle exports would remain a function of the performance and direction of global markets. Vehicle exports to Europe, Australasia, the United States, Asia and South America were expected to show further upward momentum.

The general expectation in the industry was that domestic new vehicle sales would remain fairly flat going into 2017. NAAMSA remained hopeful, however, that on the back of the expected improvement in key economic indicators, domestic sales would regain some traction in the second half of 2017 with year over year growth perhaps settling in the 2.5% to 3.5% range and hold to around that level going forward.

Factoring in the expected improvement in exports, domestic production of motor vehicles in South Africa was expected to show an increase from 604 000 vehicles produced in 2016 to close on 641 000 vehicles in 2017 – an improvement in vehicle production of about 6.0%. This figure could prove conservative if vehicle exports expand more than currently anticipated.

The projected higher vehicle production was consistent with the official vision for the Industry which is to remain a premier supplier of high quality, competitive automotive original equipment parts and accessories and vehicles to international markets and in the process, to achieve an annual domestic vehicle production figure of close to 850 000 vehicles by 2020.

Internationally and domestically, vehicle manufacturers would continue to focus on new models and products through sustained investment and new technologies. Technologies such as artificial intelligence could begin to reflect a tangible impact across sectors. Autonomous vehicles and driver assisted automatic systems as well as increased use of information technology in vehicles were likely to feature in the future.

The two companies already introduced the so-called mothership concept back in September 2016. The concept combines the advantages of a van with those of an autonomous delivery robot. A Sprinter presented as a prototype serves as a mobile loading and transport hub for eight robots.

Thanks to the intelligent interlinking of delivery processes, it will play a part in significantly improving the efficiency of last-mile delivery logistics in future. The mothership concept is the first outcome of a research and development cooperation between Mercedes-Benz Vans and Starship Technologies that began in 2016. Through its financial commitment to Starship Technologies, Mercedes-Benz Vans is now reinforcing this strategic, long-term collaboration.

“The robot can only travel short distances under its own power and until now has had to return to the warehouse to be reloaded after each delivery. On the one hand, the introduction of the van as a mobile hub widens the operational radius of the robots significantly, while also rendering superfluous the cost-intensive construction and operation of decentralized warehouses. We see the combination of these two technologies as an opportunity to give our van customers access to some completely new services and business models. At the same time, we make the delivery process much more convenient for the end customer”, says Volker Mornhinweg, Head of Mercedes-Benz Vans. “For example, the concept makes it much easier to deliver goods to the end customer on time.”

Systematic development

The aim is to develop the concept systematically over the coming months. As the two companies recently announced at CES 2017 in Las Vegas, initial pilot tests for this combination of van and robot are planned for Europe. Following pilot testing of the delivery robots, which has been and continues to be undertaken by Starship Technologies with other partners, the plan is to begin widespread testing of the joint concept with one or several logistics partners. The launch of the pilot project in a real-world environment is scheduled to take place later this year.

Mercedes-Benz Vans presses ahead with the transformation of the transport sector

Mercedes-Benz Vans unveiled its strategic future initiative adVANce last September. The business division is systematically directing its focus at new, quickly changing customer needs, with a particular eye to identifying innovative solutions. The company will invest some 500 million euros in the advancement of digitization, automation and robotics in vans as well as in innovative mobility offerings until 2020. Mercedes-Benz Vans is thus evolving from a globally successful van manufacturer into a supplier of holistic system solutions.

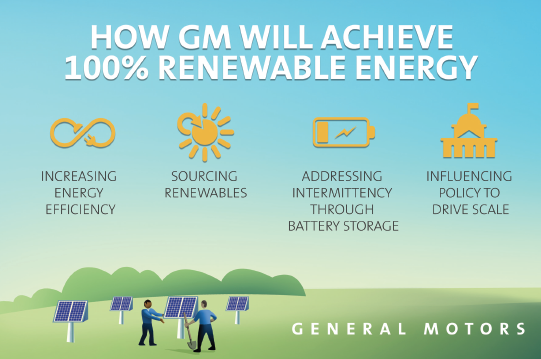

General Motors plans to generate or source all electrical power for its 350 operations in 59 countries with 100 percent renewable energy — such as wind, sun and landfill gas by 2050.

“Establishing a 100 percent renewable energy goal helps us better serve society by reducing environmental impact,” said GM Chairman and CEO Mary Barra. “This pursuit of renewable energy benefits our customers and communities through cleaner air while strengthening our business through lower and more stable energy costs.”

This new renewable energy goal, along with the pursuit of electrified vehicles and efficient manufacturing, is part of the company’s overall approach to strengthening its business, improving communities and addressing climate change. GM is also joining RE100, a global collaborative initiative of businesses committed to 100 percent renewable electricity, working to increase demand for clean power.

In 2015, GM required 9 terawatt hours of electricity to build its vehicles and power its offices, technical centers and warehouses around the world. To meet its new renewable energy goal, GM will continue to improve the energy efficiency of its operations while transitioning to clean sources for its power needs.

Today GM saves $5 million annually from using renewable energy, a number it anticipates will increase as more projects come online and the supply of renewable energy increases. In addition, the company anticipates costs to install and produce renewable energy will continue to decrease, resulting in more bottom-line returns.

The new renewable energy commitment builds on GM’s previous goal to promote the use of 125 megawatts of renewable energy by 2020. The company expects to exceed this when two new wind projects come online later this year to help power four manufacturing operations.

“This bold and ambitious commitment from General Motors will undoubtedly catch the attention of the global automotive industry,” said Amy Davidsen, North America executive director at The Climate Group. “GM has already saved millions of dollars by using renewable energy, and like any smart business that recognizes an investment opportunity, they want to seize it fully. We hope that through this leadership, other heavy manufacturing companies will be inspired to make the switch too.”

Scaling the commitment

GM is in the process of adding 30 megawatts of solar arrays at two facilities in China. Its Jinqiao Cadillac assembly plant in Shanghai will feature 10 megawatts of rooftop solar and 20 megawatts of solar carports, which will cover 8,100 parking spaces at the company’s vehicle distribution center parking lot in Wuhan.

GM has pioneered the use of renewable energy for more than 20 years, saving $80 million to date. The company has 22 facilities with solar arrays, three sites using landfill gas and four that will soon benefit from wind. This experience will help GM scale renewable energy use to all facilities globally.

GM is in a unique position to meet this renewable energy goal given its electric vehicle battery expertise. Energy storage can ultimately address the intermittency or reliability of wind and solar energy. GM is now using Chevrolet Volt batteries for energy storage at its Milford Proving Ground data center office.

Collaborating to make renewable energy more accessible

GM joins 69 companies that have made the RE100 pledge. As a founding member of the Renewable Energy Buyers Alliance and Business Renewable Center, and one of the first signatories of the Renewable Energy Buyers’ Principles, GM helps scale the availability and adoption of renewable energy. These organizations, spearheaded by the Rocky Mountain Institute, the World Wildlife Fund and the World Resources Institute, work to identify barriers to buying clean energy and develop solutions to meet the growing demand.

GM will continue to work with cities, policymakers, renewable energy developers, utilities, NGOs and other stakeholders on the transition to a clean-energy economy.

Volkswagen is forging ahead with the regionalization of its worldwide automobile business and recently inaugurated a vehicle production facility in Kenya. Together with the President of Kenya, H.E. Uhuru Kenyatta, Dr. Herbert Diess, CEO of the Volkswagen brand, was present when the first locally produced Polo Vivo rolled off the production line. With the CKD production of the bestselling car model in the sub-Saharan region, Volkswagen is stepping up its commitment to Africa. This is a key step in the development of new opportunity markets – with the right products, local partners and training in the region.

At the inauguration, Diess underlined Kenya’s key role within the Volkswagen brand’s Africa strategy, “Volkswagen is strengthening the production region of Africa and providing additional impetus for the further regionalization of the brand – as a reliable and responsible partner. This is symbolized by the first Polo Vivo produced – a car from Africa for Africa.” Diess also said, “here in Kenya, we will be producing cars that bear comparison with European quality standards. This is why we are opting for training and local skills in automobile production.”

In addition to vehicle production, Volkswagen will be offering Kenyan customers a comprehensive package including a manufacturer’s guarantee as well as a maintenance and service plan. Financing schemes will be developed together with local banks in order to allow individual mobility and to provide Volkswagen with the impetus it needs for its re-entry to the Kenyan market.

President Kenyatta said, “a few months ago, this was only a dream. Now Volkswagen’s investment in Kenya has become reality. This is further proof of my government’s determination to strengthen the production location of Nairobi and to forge ahead with the industrialization of the nation.”

Third Volkswagen production plant in Africa

The joint project implemented together with DT Dobie in Thika near to the Kenyan capital Nairobi is Volkswagen’s third production plant in Africa, together with one plant in South Africa and one in Nigeria. In the initial phase, annual production of up to 1,000 vehicles is planned. In the long term, it will be possible to produce up to 5,000 units per year at the plant of Kenya Vehicle Manufacturers (KVM). The assembly facility is flexibly designed and offers the possibility of investigating the production of further models in the event of positive developments in the new car market. In addition, the Volkswagen Group recently announced plans to start vehicle production in Algeria.

Volkswagen committed to sustainable training in Kenya

For the start of production at Thika, the employees are being trained by Volkswagen Group South Africa. This will ensure that all vehicles have constant high quality levels. Volkswagen is also investigating possible approaches for the establishment of a sustainable, practically oriented training initiative.

Apart from school or academic training, young people are also to receive practical training in order to improve their employment prospects in the region as a whole.

Kenya is an opportunity market in Africa. The country has an outstanding position within the region of East Africa and has the most powerful economy in the East African Community (EAC) with a GDP of about US$63 billion. In addition, Kenya is a key transit country for trade throughout East Africa. The good economic relations between Kenya and Germany are also being continuously and strategically expanded by the governments concerned.

Volkswagen and Kenya – this is a relationship with a tradition – Volkswagen already assembled the Beetle in Kenya in the 1960s. The Volkswagen brand is now returning to Kenya with its first model, the Polo Vivo.

At its busy open house in High Wycombe during December 2016 and in the immediate aftermath, Hurco Europe took orders for 12 vertical machining centres to the value of £800,000. The company welcomed 70 engineers from 50 manufacturing companies from the OEM and subcontracting sectors during the two-day show.

The event cemented a solid start to the current financial year, beginning 1st November, since when over 70 orders have been booked, double the number compared with the same period last year.

Managing director David Waghorn said, “trading was quiet in the run-up to Brexit, but business has picked up strongly since late summer and it looks set to continue into 2017. Our 2015/16 turnover was just short of £20 million, the fifth successive year it has been very close to that figure.

“We launched our new, entry-level VM5i machining centre in September and sold 10 before our open house, which helped to boost turnover in both financial years.

“The proportion of new companies buying Hurco equipment in 2015/16 was just over 40 percent, similar to the last five years, which is the reason we have been able to sustain our business growth.”

A further explanation for the near-record level of trading last year was the sale of five German-built Roeders 5-axis machining centres with automation into the UK and Ireland under a sole agency agreement. Virtually all models in the Roeders machining centre range can be equipped with jig grinding at 90,000 rpm. The option is creating considerable interest presently in the motorsport and automotive sectors.

Sales of Hurco’s own 5-axis machining centres are also holding up well, with the VMX42SRTi and VMX60SRTi B-axis models with flush rotary table proving most popular, although trunnion-type configurations are preferred for some applications.

Hurco’s large, high-value DCX bridge-type machining centres have contributed well to the bottom line. Mr Waghorn advised that a 5-axis variant of the DCX32 is currently being installed and announced that a DCX62 with 6.2 metre X-axis is now available, built to order. There are over 20 DCX-series machines operational in the UK.

Another factor that raised turnover in 2016 was a propensity for customers to enhance their machine specification with, for example, extra rotary axes, higher spindle speeds, full swarf management, through-tool coolant and probing for parts and tools.

Hurco has been selling machining centres for the whole year with its latest MAX 5 control system, which has proved highly popular. Running the latest WinMAX 10 software, it is ideal for conversational programming of 5-sided and 4th axis rotary cutting cycles, but also handles all of the latest ISNC codes required to run simultaneous 5-axis programs.

Unlike previously, a customer can take delivery of a VM-series machining centre with a single-screen MAX control and upgrade it later to a twin-screen version with the addition of a hinged, 19-inch LCD screen, as supplied with VMX- and DCX-series machines. The operator can then view an image of the part as the cycle is being built up conversationally or monitor a machining process while the next job is being programmed.

Products and services from a larger number of partner companies than ever were promoted at the open house. They included workholding equipment suppliers 1st MTA and Roemheld, probing systems firm Renishaw, tooling suppliers Horn, Kyocera SGS, Dormer Pramet, Gewefa and Coventry Engineering, tool presetter company Zoller, CNC bar feed firm Hydrafeed, filtration equipment specialist Filtermist, CADCAM solution providers Autodesk, Edgecam and Open Mind, Erowa automation system agent REM Systems, Anotronic with its new River 3 EDM drill, Finance For Industry and Cromwell, a supplier of cutting tools, abrasives and power tools as well as products for factory maintenance and repair.

“The robot can only travel short distances under its own power and until now has had to return to the warehouse to be reloaded after each delivery. On the one hand, the introduction of the van as a mobile hub widens the operational radius of the robots significantly, while also rendering superfluous the cost-intensive construction and operation of decentralized warehouses. We see the combination of these two technologies as an opportunity to give our van customers access to some completely new services and business models. At the same time, we make the delivery process much more convenient for the end customer”, says Volker Mornhinweg, Head of Mercedes-Benz Vans. “For example, the concept makes it much easier to deliver goods to the end customer on time.”

“The robot can only travel short distances under its own power and until now has had to return to the warehouse to be reloaded after each delivery. On the one hand, the introduction of the van as a mobile hub widens the operational radius of the robots significantly, while also rendering superfluous the cost-intensive construction and operation of decentralized warehouses. We see the combination of these two technologies as an opportunity to give our van customers access to some completely new services and business models. At the same time, we make the delivery process much more convenient for the end customer”, says Volker Mornhinweg, Head of Mercedes-Benz Vans. “For example, the concept makes it much easier to deliver goods to the end customer on time.”

In 2015, GM required 9 terawatt hours of electricity to build its vehicles and power its offices, technical centers and warehouses around the world. To meet its new renewable energy goal, GM will continue to improve the energy efficiency of its operations while transitioning to clean sources for its power needs.

In 2015, GM required 9 terawatt hours of electricity to build its vehicles and power its offices, technical centers and warehouses around the world. To meet its new renewable energy goal, GM will continue to improve the energy efficiency of its operations while transitioning to clean sources for its power needs.