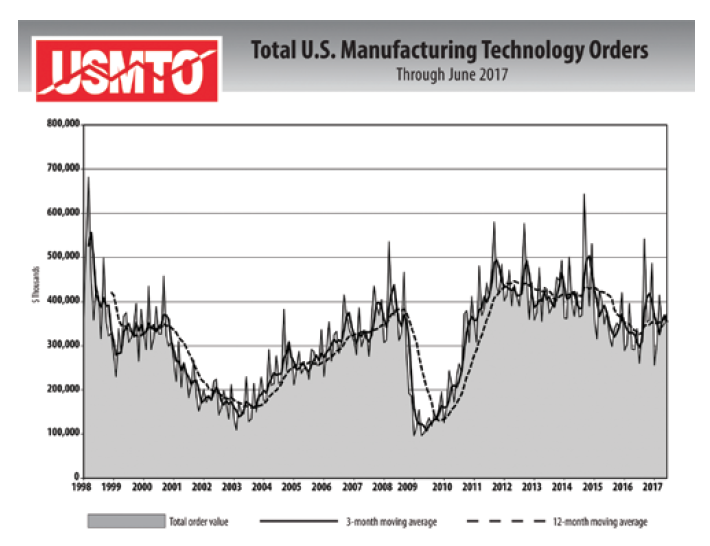

June manufacturing technology orders climbed 6.5 percent over May, according to a report released by AMT – The Association For Manufacturing Technology.

The latest U.S. Manufacturing Technology Orders (USMTO) report also shows a year-over-year increase of more than 10 percent, the fifth consecutive month posting a year-over-year gain.

The U.S. manufacturing technology market has been weak since oil prices began to drop dramatically in June 2014. Orders peaked on a monthly basis that September at $643 million and bottomed out at $260 million in June 2016. IMTS – The International Manufacturing Technology Show, held in September 2016, rekindled the market, but it was not until March 2017 that year-overyear numbers began to consistently show a positive, accelerating trend upwards. Now, three months later, June figures are up 10 percent over June 2016 and represent the volume and growth that supports an announcement that the manufacturing technology market is officially expanding.

“If the USMTO numbers aren’t convincing enough that a recovery is underway, certainly the buzz among our members underscores that a recovery is indeed underway,” said AMT President Doug Woods. “Members have shared that the aerospace supply chain in the Midwest is hot, auto orders doubled between May and June and sales in the Southeast exploded. Over the next six months, they look forward to a broadening of the recovery into areas like agricultural, construction, power generation and off-road machinery industries.”

The USMTO data supports the anecdotal evidence from AMT members. Automotiverelated orders were up 109 percent from May and the aerospace industry’s bookings of new production technology were up 47 percent. While the largest growth by any region is the 42 percent increase in orders originating in the states from Tennessee north to Michigan, the Southeast and West are posting the fastest growth rates yearto- date in manufacturing technology orders.

Key indicators that businesses in the manufacturing technology sector rely on have been improving steadily. Housing starts are an important indicator of trends as every new house has at least seven new appliances, a car in the driveway, and a consumer or two with disposable income.

In June, housing starts topped 1.2 million which isn’t at peak levels but continues an upward trend in the indicator. The increase goes hand-in-hand with the continuing strength of consumer confidence which, according to the University of Michigan’s Consumer Confidence, has been over 90 since September 2016.

It isn’t only the consumer that is fostering growth in the need for additional manufacturing capacity. USMTO tracks well with the Purchasing Managers’ Index (PMI) produced by the Institute of Supply Management. Any mark over 50 represents an expansion and the index is 56.3 in July, up from the June level. Business’ profitability over the past three quarters primes the pump for expansion on corporate investment in new durable goods and production equipment.

Mark Killion, Director of U.S. Industries for Oxford Economics, noted, “Recent increases in new orders for machine tools are supported by a better environment for business investments in the U.S. and globally, especially in the sectors for metals products, electrical and industrial machinery.”

AMT has recently replaced one of its key indicators with the Gardner Business Index (GBI) which tracks well with USMTO and turned upwards markedly in December 2016, about 90 days before the recognizable upturn in USMTO.

“As we expected, machine tool orders have performed well in recent months. The backlog index from the GBI: Metalworking bottomed out in January 2016. The backlog index tends to lead machine tool consumption by 14 to 20 months. Since the backlog is still growing at an accelerating rate, we expect solid growth in machine tool orders through at least the end of 2017,” commented Steve Kline, Director of Market Intelligence, Gardner Business Media and creator of the GBI.

Leave your vehicle to park itself. Daimler and Bosch have teamed up to realise driverless parking (Automated Valet Parking) in the multi-storey car park at the Mercedes-Benz Museum in Stuttgart.

Cars now proceed without a driver to their assigned parking space in response to a command issued by smartphone, without any need for the driver to supervise the manoeuvre. Automated valet parking marks an important milestone on the way to autonomous driving. The pilot solution at the multi-storey car park of the Mercedes-Benz Museum represents the world’s first infrastructure-supported solution for an automated drive-up and parking service in real-life dual operating mode. From the beginning of 2018, visitors to the museum’s multi-storey car park will be able to experience the convenient service at first hand and avoid spending time parking their cars.

“We are approaching autonomous driving faster than many people suspect. The driverless parking solution at the Mercedes- Benz Museum demonstrates in impressive fashion just how far the technology has come,” said Dr Michael Hafner, Head of Automated Driving and Active Safety at Mercedes-Benz Cars Development. “Parking will be an automated process in the future. By applying an intelligent multi-storey car park infrastructure and networking it with vehicles, we have managed to realise driverless parking substantially earlier than planned,” said Gerhard Steiger, Director of the Chassis Systems Control unit at Bosch.

To the parking space and back – fully automatically

Anyone can reserve a car using a smartphone app. The vehicle rolls into the pick-up area autonomously to start the journey. The return procedure is equally convenient: the customer parks the vehicle in the car park’s drop-off area and hands it back by smartphone app. After being registered by the intelligent system installed at the multistorey car park, the car is started and guided to an assigned parking space.

Driverless parking is made possible by an intelligent multi-storey car park infrastructure from Bosch in conjunction with the vehicle technology from Mercedes-Benz. Sensors installed in the car park monitor the driving corridor and its surroundings and steer the vehicle. The technology on board the car performs safe driving manoeuvres in response to the commands from the car park infrastructure and stops the vehicle in good time when necessary. The sensors for the multi-storey car park infrastructure and the communications technology come from Bosch. Daimler is providing the private museum car park and pilot vehicles, defining the interface between infrastructure and vehicle together with Bosch and adapting the sensor technology and software in the vehicles accordingly.

First operating licence worldwide for driverless parking

The premiere on 24 July 2017 is to be followed by an extensive trial and commissioning phase. The project has been overseen from the outset by local authorities – Stuttgart regional council and the federal state transport ministry – and by appraisers from the TÜV Rheinland technical inspection authority with the aim of assessing the safe operation of the vehicle and car park technology. Before the driverless customer service goes into operation at the beginning of 2018 – as the first such application worldwide – final approval will be required from the licensing authority.

Everything will then be in place to enable automated valet parking to be made available to everyone at the Mercedes-Benz Museum’s multi-storey car park from the beginning of 2018. Bosch and Mercedes-Benz intend to use this project to acquire experience regarding users’ handling of automated valet parking. Other existing multi-storey car parks can be retrofitted with the infrastructure technology. For the operators of multi-storey car parks, driverless parking means more efficient use of the available parking space: up to 20 percent more vehicles fit into the same space.

Electrification is one of the central pillars of the BMW Group’s corporate strategy NUMBER ONE > NEXT and the company has announced that all brands and model series can be electrified, with a full-electric or plug-in hybrid drivetrain being offered in addition to the combustion engine option.

Additional electrified models will be brought to market in the coming years and beyond 2020, the company’s next generation vehicle architecture will enable further fully-electric vehicles.

Recently, the BMW Group announced that the new battery-electric MINI will be a variant of the brand’s core 3 door model. This fully electric car will go into production in 2019, increasing the choice of MINI powertrains to include petrol and diesel internal combustion engines, a plug-in hybrid and a battery electric vehicle. The electric MINI’s electric drivetrain will be built at the BMW Group’s e-mobility centre at Plants Dingolfing and Landshut in Bavaria before being integrated into the car at Plant Oxford, which is the main production location for the MINI 3 door model.

Oliver Zipse, BMW AG Management Board member for Production said, “BMW Group Plants Dingolfing and Landshut play a leading role within our global production network as the company’s global competence centre for electric mobility. Our adaptable production system is innovative and able to react rapidly to changing customer demand. If required, we can increase production of electric drivetrain motor components quickly and efficiently, in line with market developments.”

By 2025, the BMW Group expects electrified vehicles to account for between 15-25% of sales. However, factors such as regulation, incentives and charging infrastructure will play a major role in determining the scale of electrification from market to market. In order to react quickly and appropriately to customer demand, the BMW Group has developed a uniquely flexible system across its global production network. In the future, the BMW Group production system will create structures that enable our production facilities to build models with a combustion engine, plug-in hybrid or fully electric drive train at the same time.

The BMW Group currently produces electrified models at ten plants worldwide; since 2013, all the significant elements of the electric drivetrain for these vehicles come from the company’s plants in Dingolfing and Landshut. Dingolfing additionally builds the plug-in hybrid versions of the BMW 5 Series and the BMW 7 Series and from 2021, it will build the BMW i NEXT. The BMW Group has invested a total of more than 100 million euros in electro-mobility at the Dingolfing site to date, with investment continuing as the BMW Group’s range of electrified vehicles further expands.

Electrification of all brands and model series continues

The new, fully-electric MINI is one of a series of electrified models to be launched by the BMW and MINI brands in the coming years. In 2018, the BMW i8 Roadster will become the newest member of the BMW i family. The all-electric BMW X3 has been announced for 2020 and the BMW iNEXT is due in 2021.

Today, the BMW Group offers the widest range of electrified vehicles of any car manufacturer in the world, with nine models already on the market. These range from the fully-electric BMW i3 to the company’s newest electrified model, the MINI Cooper S E Countryman ALL4, a plug-in hybrid version of the MINI Countryman, which is produced by VDL Nedcar in the Netherlands. The company has committed to selling 100,000 electrified vehicles in 2017 and will have a total of 200,000 electrified vehicles on the roads by the end of the year.

The BMW Group has benefited from its early start on the road to electrification. Indeed, the company’s pioneering, large scale electric vehicle trial began world-wide in 2008 with the MINI E. Learnings from this project played a crucial role in the subsequent development of the BMW i3 and BMW i8, technology pioneers which themselves informed the company’s current range of plug-in hybrid vehicles.

Composite materials have been called the shape of aerospace’s future. With their winning combination of high strength, low weight and durability, it’s easy to see why.

For more than 30 years, Airbus has pioneered the use of such materials in its commercial jetliners, from the cornerstone A310’s vertical stabilizer to today’s A350 XWB – on which more than half of the aircraft’s structure is composite.

In essence, a composite material is made from two or more constituent materials with different physical or chemical properties. When combined, the composite material exhibits beneficial physical characteristics quite different from what the individual components alone can provide. Commonlyrecognized composites in everyday life include plywood and reinforced concrete.

From nose to tail, Airbus utilizes advanced composites in its jetliner product line that have been at the forefront of materials science. One particular standout material is carbon-fibre reinforced plastic, or CFRP. Composed of carbon fibres locked into place with a plastic resin, CFRP offers a better strength-to-weight ratio than metals and has less sensitivity to fatigue and corrosion. In short, it’s lighter than aluminium, stronger than iron and more corrosion-resistant than both.

Like all composites, the strength of CFRP results from the interplay between its component materials. By themselves, neither the carbon fibres nor the resin is sufficient to create a product with the desired characteristics to be integrated on an aircraft. But once combined in multiple, integrated layers and bonded, the CFRP airframe component or aerostructure takes on the strength and load-bearing properties that make it ideal for aviation use.

The application of carbon-fibre reinforced plastic reached new proportions with the A350 XWB, which boasts a significant application of composites throughout. For example, most of the A350 XWB’s wing is comprised of the lightweight carbon composites, including its upper and lower covers. Measuring 32 metres long by six metres wide, these are among the largest single aviation parts ever made from carbon fibre.

With CFRP, not only is the jetliner’s airframe tougher and stronger, the reduction in weight enables it to carry more passengers, burn less fuel, fly farther…or combinations of the three.

While initially more expensive to produce than traditional metallic parts, CFRP components can save aircraft operators money on future maintenance costs since the material doesn’t rust or corrode. An A350 XWB, for example, requires 50% fewer structure maintenance tasks and the threshold for airframe checks is at 12 years compared to eight for the A380.

In CFRP production, thousands of microscopically thin carbon threads are bundled together to make each fibre, which joins others in a matrix held together by a robust resin to achieve the required level of rigidity. The composite component is produced in precisely shaped sheets laid atop each other and then bonded, typically using heat and pressure in an oven called an autoclave, resulting in a high quality composite.

Parts such as fuselage and wings can make extensive use of composites as the required fibre loading – the way the fibres are laid up and cured in the autoclave – is simple. However, parts requiring complex loading will, for the foreseeable future, continue to use metal.

The two most commonly used types of CFRP are thermoset and thermoplastic. While thermoset CFRPs are currently more widespread in the aeronautics industry, thermoplastics are gaining popularity because of their recyclability – an important lifecycle consideration that has long been a factor against wider CFRP adoption.

A key difference between thermoset and thermoplastic materials is what happens during the curing process. When cured in the autoclave, thermoset material undergoes a chemical reaction that permanently changes its makeup. A thermoplastic part, though, can be re-melted and still maintain its composition.

That difference makes thermoplastics attractive since Airbus and its suppliers produce hundreds of tonnes of scrap composites each year. While scrap thermoset resin cannot be reused, thermoplastic scrap can be used in a variety of ways and in a number of sectors beyond aeronautics.

Governments and industry stakeholders are keenly following developments in the microelectronics industry, as these technologies could potentially disrupt and bolster the Internet of Things (IoT) Mega Trend.

Microelectronics will support eco-friendliness, Innovating to Zero, smart and connected homes, cloud computing and miniaturization trends and influence the technological progress of a wide range of industries. This will open up opportunities across value chains and key industry participants are actively entering this technology space to gain an early mover advantage.

“One of the major selling points of microelectronics is its low power consumption. Industries recognize that the technology’s rapid charging, smart antenna, wireless charging and organic light-emitting diodes (OLEDs) make it extremely cost effective in the long term,” noted Frost & Sullivan TechVision Research Analyst Brinda Manivannan. “Furthermore, a small footprint makes microelectronics relevant in an era that is experiencing the accelerated adoption of wearables and smart devices. Wireless communication technologies and display technologies will be significantly affected by this trend.”

Top Technologies in Microelectronics, 2017 is part of Frost & Sullivan’s TechVision (Microelectronics) Growth Partnership Service programme. The study assesses the impact of the top emerging microelectronics technologies, the innovation strength of each region and the global market potential of the technology. It also covers the dynamic technologies that enable the convergence of Mega Trends such as smart cities, vehicle to X (V2X) systems, IoT and connected systems.

While the benefits of microelectronics are manifold, scientists and adopters are still challenged by the huge cost of research and development (R&D), capital-intensive manufacturing, scalability limitations, volume production and lack of a structured supply chain. However, technology developers are gradually addressing these roadblocks to adoption, with North America leading in technology advancements and Asia-Pacific in technology adoption.

“Microelectronics R&D will also get a boost with the impending bandwidth crunch due to the increased penetration of augmented reality and virtual reality devices. Microelectronics can be employed to develop faster data transmission technologies such as visible light communication (VLC) and advanced data storage techniques to power data-intensive applications,” noted Manivannan. “Meanwhile, the evolution of display technologies from conventional liquid crystal display to flexible and highly versatile OLED technology is also accelerating the need for microelectronics, ensuring a steady stream of innovations from visionary industry participants.”

About TechVision

Frost & Sullivan’s global TechVision practice is focused on innovation, disruption and convergence, and provides a variety of technology-based alerts, newsletters and research services as well as growth consulting services. Its premier offering, the TechVision programme, identifies and evaluates the most valuable emerging and disruptive technologies enabling products with near-term potential. A unique feature of the TechVision programme is an annual selection of 50 technologies that can generate convergence scenarios, possibly disrupt the innovation landscape, and drive transformational growth.

The whole world is talking about 3D printing, additive manufacturing and generative multi-layer construction technologies.

To quote Carl Fruth, Managing Board Chairman of FIT AG, Lupburg, “at EMO, the very latest CNC-based production technologies will be on show, additive manufacturing among them. Innovative potential product solutions in this field will be demonstrated.” Photo: Fit AG

Nevertheless, this is a long way from meaning that the classical machine tool is going to be pensioned off. EMO Hannover 2017 will be showcasing an international banquet of production technology – with alternative processes as the highly auspicious icing on the cake.

Carl Fruth has meanwhile long since achieved his goal of transferring competences in the field of multi-layer technologies into product manufacturing: moreover, within the framework of a Technology Day featuring an in-house exhibition held in April 2017, FIT AG (Fruth Innovative Technologies) in the Upper Palatinate village of Lupburg, in addition to inaugurating a new office building also opened the first additive factory. The “FIT factory is even on an international comparison unique in terms of manufacturing capacity and automation technology, and is intended to serve as a template for further additive manufacturing facilities of the FIT Group,” to quote the firm’s founding father and Managing Board Chairman Fruth. He is a pioneer of additive manufacturing – and a visionary for whom ten years ago it was already a certainty that multi-layer construction technology would in future be the norm in everyday production operations and the sales of milling machines or injection moulding machines would inexorably decline.

But that is still a long way from meaning that the days of the mother of all machines (i.e. the traditional machine tool) are numbered. This is impressively confirmed by the innovations that will be showcased by the exhibitors at EMO Hannover 2017. One of the impediments to the widespread adoption of additive technology in individualized mass production was described several years ago by Fruth himself as the lack of productionsuited manufacturing lines. This has changed in the meantime. Fruth puts it like this: “There are a large number of delicate seedlings: many of our customers would like to use additive technologies to manufacture replacements for existing components. But this is possible only in a very few cases. Usually, a new component has to be developed and very often the adjoining components of the system as well. Firstly, many companies are deterred by the outlay involved, and secondly, of course, you need specialized development competence for this new production technology.”

The country needs new designer engineers

When traditional design guidelines no longer apply, a new generation of design engineers is needed, keen to embrace function-driven thinking. According to Fruth, additive manufacturing means that in the design phase not only the geometry, but also the material properties and the component costs are essentially specified in full. This complexity necessitates specialized training and experience. Moreover, up to now there is no software tool in existence that provides all the requisite functions. So firms have to work with different, complex software tools. Very often, information is lost in transitioning from one tool to another. When you need up to eight iterations for developing a component, the substantial outlay involved is obvious.”

˝The competences required, moreover, are possessed not by a single design engineer, but only by a team. In traditional companies, furthermore, the competences concerned are divided up among different departments – a situation exacerbated by squabbles about prerogatives and uncertainty. Innovative companies, however, also see this as an opportunity: “we support our customers in this process, and train them component by component to achieve maximized performance in AM design. That’s why we also call these products ADM – Additive Design and Manufacturing”.

When the talk turns to additive manufacturing in an automated process chain (something he used to refer to as the Achilles’ heel!), Fruth becomes veritably effusive, “this is my own particular hobbyhorse. We don’t have a digital specification of our products. This is why Industry 4.0 hasn’t taken off and also why automation isn’t working properly either. When everything has to be automated and optimized by hand, then the traditional forms of mass production are – old hat!” Whether there’s a robot standing at the production line or a human employee turning the product, there are no fundamentally new approaches involved: “For as long as a drawing and thick ring binders of text are required for specifying a product, Industry 4.0 is never going to get off the ground. In this context, it’s immaterial whether there’s a PDF file for the specification involved – we’re talking here about machine-readable specifications and their fully automated implementation.” Some former weak points, by contrast, he adds, like the reproducibility of the processes, quality assurance in mass production, or dependable simulation methods, have been almost eliminated. “Everyone involved has understood the problem and is working purposefully to solve it.”

More technologies are sharing the market

To quote Peter Scheller, Marketing Director at Siemens PLM Software, Cologne, “EMO Hannover 2017 is an excellent platform for learning more about ongoing challenges and customers’ wishes.” Photo: Siemens PLM

The inevitable question of whether the conventional machine tool will soon be out of a job receives a differentiated answer from the AM expert. “Components are manufactured in a process chain. That’s true today and will still be true tomorrow. Additively manufactured components, as is the case with other production technologies, too, require quality-testing – it’s immaterial in this context whether this means each individual component or every 50th one of identical components. So I don’t think existing technologies are going to be replaced.” CNC-driven processes, he adds, are all very flexible in use, and all have a market of their own. The question is rather, “what share can each technology have of the cake as a whole?” The slice for the various additive production technologies is currently so small that it can only increase. Fruth, however, also believes that the cake as a whole for CNC processes is becoming larger, at the expense of tool-linked production technologies and other highly personnelintensive processes. We’re looking here at a combination of different CNC technologies.

At the upcoming EMO Hannover 2017, Fruth expects “to find the very latest CNC-based production technologies, plus innovative potential products in this category. A large number of equipment manufacturers for additive processes and material producers will be exhibiting at EMO Hannover. For us as users of this equipment, this adds a special interest to the fair.”

Harmonized software solutions for additive manufacturing

A new solution for additive manufacturing has recently been premiered by Siemens PLM Software, the Business Unit for Product Lifecycle Management (PLM), Cologne. It consists of an integrated software package for design, simulation, digital manufacturing, plus data and process management. This enables a generative design to be created automatically, on the basis of new functions for optimised topologies. This frequently results in organic shapes that a design engineer would be highly unlikely to think of himself, and that would be very complicated or even impossible to manufacture using conventional production methods. Possible user target groups include the automotive industry, the aviation sector or medical technology.

The revolutionary solution and its possible applications are explained by Peter Scheller, Marketing Director at Siemens PLM Software. “What’s special about it is that this is a consistently harmonized platform. On the basis of our Convergent Modelling technology, we incorporate within our NX software for integrated CAD all the relevant product development steps for 3D printing, from scanning to the actual printing. In the field of 3D printing, there are already a whole lot of individual solutions in various niches, either from printer manufacturers or other vendors. The important step we’re now taking is the integration of all process steps into a platform with a central user interface, on which both the geometry and the print path generation are stored in a secure data format.”

Highly sophisticated integrated technologies for simulations and analyses enable a design’s behaviour to be calculated in advance. This new technology, with its high change triggering potential, will encourage innovative design approaches. Photo: Siemens PLM

In addition, within the framework of this strategy, Siemens PLM Software has unveiled plans for a new online collaboration platform providing an option for worldwide cooperation in the manufacturing sector. The declared aim is to render on-demand product designs and 3D printing production operations more easily accessible to a global manufacturing industry. In mass production environments,” says Scheller, “3D printing has not yet arrived completely: it originated in prototyping and so far has been predominantly used for this purpose. But we’re approaching a threshold here: the process is emerging from this niche; many companies are currently thinking about using it for mass production or have already introduced it for this purpose.” When you think about an additive production process on an industrial scale, “from our point of view a processreliable data format is extremely important, as a basis for enabling components to be dependably manufactured again and again in the same quality. So far there hadn’t been a platform of this kind, which is why we’re now providing one for our customers.” For industrial production operations, in particular, it is very important to have an exhaustive description of your components on file in digital form. This is essential for accessing this digital twin in the event of queries or cases of damage and investigating the relevant causes.

Scheller sums up his expectations for EMO Hannover 2017 as follows: “Siemens will continue to invest in innovations and to work together with technology partners in order to develop new solutions designed to progress the efficacy of additive manufacturing and drive 3D printing forward still further. That’s why we’re looking forward to fruitful meetings at EMO Hannover 2017 and plenty of mutual feedback with customers and associates. The fair is a superlative platform for learning more about current challenges and customers’ wishes.”

The employment figures released by Statistics South Africa (StatsSA) indicate a deeply troubled economy which, in the absence of a solution, will see ordinary South Africans continuing to suffer badly, the Steel and Engineering Industries Federation of Southern Africa (SEIFSA) said.

SEIFSA Senior Economist Tafadzwa Chibanguza.

SEIFSA Senior Economist Tafadzwa Chibanguza said that given the 2017 firstquarter Gross Domestic Product (GDP) figures recently published, which revealed that South Africa had fallen into a recession, it almost seemed a forgone conclusion that the employment figures for the same period would confirm a negative picture.

“In fact, the employment figures mirror those of the GDP, with the tertiary services contributing the most to the employment declines,” Chibanguza added.

The quarterly employment statistics released by StatsSA showed that a total of 48 000 jobs were lost between the fourth quarter of 2016 and the first quarter of 2017, amounting to a 0.5% decrease. Between the first quarter of 2016 and the first quarter of this year, a total of 58 000 jobs – representing 0,6% of jobs – were shed.

The 48 000 jobs lost in Q1 2017 is a net number, which is the result of decreases in most sectors and increases in some. Chibanguza said if all the jobs lost in the tertiary sector were added up, then a total of 64 000 jobs were lost between the end of Q4 2016 and Q1 2017.

If the 4000 jobs lost in the manufacturing sector were added, then a total of 68 000 jobs were lost in Q1 2017. Chibanguza said that, with employment being an outcome variable which increases or decreases on the back of higher or lower levels of economic activity, South Africa “a thorough introspection of its challenges in order for meaningful solutions to be found”.

He said that it was encouraging to note that the mining sector had added 8000 jobs and the construction sector 12 000 jobs in Q1:2017. He said that the increase in mining jobs was to be expected given the relatively better mining production statistics released for the first quarter of 2017, which was assisted by stronger commodity prices.

However, Chibanguza cautioned that the new version of the Mining Charter released by the Minister of Mineral Resources last week had the potential to undo this upside.

He added that construction employment generally tended to be volatile, depending on the number of projects in progress and sounded a caution that the current weak levels of business confidence and the accompanying slow gross fixed capital formation were likely to imperil this trend.

“Rome is burning and the man on the street is the biggest victim”, Chibanguza warned.

SEIFSA Senior Economist Tafadzwa Chibanguza said the announcement made by representatives of the National Association of Automobile Manufacturers of South Africa in Sandton recently that Original Equipment Manufacturers (OEMs) would increase their sourcing of locallyproduced goods as part of their 2035 Transformation Plan boded well for the metals and engineering sector, which was a supplier to auto manufacturers.

SEIFSA Senior Economist Tafadzwa Chibanguza.

The announcement was made after a meeting with the ANC leadership, which was also part of that press conference.

Chibanguza said that the announcement speaks directly to the metals and engineering sector, which SEIFSA represents. He said the automotive sector makes up 31% of the total demand profile of the metals and engineering sector.

“It is, in fact, the largest domestic demand source for metals and engineering products, followed by construction and then mining. Prospects to increase local sourcing of inputs translates favourably to the metals and engineering sector since it indicates a potential growing share of activity for local companies.

“This is a classic case of a dynamic and pragmatic approach to a difficult economic environment,” Chibanguza said.

He said that current levels of economic activity are very weak and only economic growth would counter that situation, but that would not happen overnight. The announcement by the automotive sector was a welcome, dynamic response to that weak environment.

Chibanguza expressed the hope that the current impasse in the mining sector occasioned by the new Mining Charter would be resolved speedily in order to improve demand levels from that sector to the metals and engineering sector.

The contraction in the metals and engineering sector will be the focus of the 3rd annual South African Metals and Engineering Indaba in September.

SEIFSA Chief Executive Officer, Kaizer Nyatsumba.

The Indaba, to be held at the Industrial Development Corporation (IDC) Conference Centre in Sandton, from 14-15 September, is set to take place against the backdrop of negative sentiment about the South African economy because of, among others, falling Gross Domestic Product (GDP) and contraction in the secondary sector in the first quarter of this year.

According to the South African Reserve Bank’s Quarterly Bulletin June 2017, manufacturing production contracted for the third successive quarter in the first quarter of this year. This was mainly due to weak domestic demand and low business confidence.

Presented by the Steel and Engineering Industries Federation of Southern Africa (SEIFSA) in partnership with the Industrial Development Corporation and the Department of Trade and Industry, the Indaba is an opportunity for business executives, policy makers and trade union representatives to collaborate towards addressing the challenges facing the sector.

Speaking ahead of the Indaba, Steel and Engineering Industries Federation of Southern Africa (SEIFSA) Chief Executive Officer, Kaizer Nyatsumba said, in addition to tackling the challenges in the sector, the conference would also consider the steps necessary to reverse the contraction in the metals and engineering sector.

According to Statistics South Africa, the metals and engineering sector has shrunk in each successive year since 2013.

“We need to urgently turn around that trend because the steel and engineering sector is an important contributor to the GDP and job creation,” Nyatsumba said.

He added, “this requires collaboration between government, labour and business. With unemployment currently at unacceptably high levels, South Africa needs a vibrant and competitive steel and engineering sector. The Indaba is an opportunity for the different stakeholders to exchange ideas.”

It is common cause that the Industry is in distress. According to the MEIBC the Industry lost 150 000 jobs over the 10 year period from 2006 to 2015.

The IDC recently confirmed a further 25 000 job losses and 500 business closures during the last twelve month period. The issue of uncompetitive wages is one of the main causes stifling job creation in the Industry.

Gerhard Papenfus, Chief Executive (NEASA)

The wages in the Steel Industry are currently, on average, double that of other Industries covered by bargaining council agreements. The wage gap is even bigger when it is compared to wages determined by wage determinations.

The wage proposal by NEASA and other employer groupings in this round of negotiations are to address this ever worsening trend in terms of job losses and also to create a position in which new jobs could be created. One of the employer demands is to establish a new entry level wage for newly appointed employees in this Industry.

In press releases by the National Union of Metalworkers of South Africa (NUMSA), they constantly create the impression that this constituted a downward variation of wages.

This is simply not true. It is not the case now, and it has never been the position of employers. In terms of the employers’ position in this regard, the wages of existing employees will not be affected.

The same applies to the misinformation being circulated to the effect that, apart from employers proposing to reduce the wages of current employees, they also want to increase working hours. Again this is not true. The proposal by employers in this regard is simply to add an additional five hours to the normal working hours before overtime is introduced.

In spreading misinformation about the employers’ proposals, knowing perfectly well that it is not true, NUMSA is playing a very dangerous game – probably aimed at inciting employees to strike – for the wrong reasons. This is dangerous, mischievous and irresponsible.

Stakeholders at the negotiating table, both employers and trade unions, must remember that they are not only negotiating for their own interests. There is indeed much more at stake. Opening the opportunity of employment to the millions of unemployed people has now become one of South Africa’s most strategic objectives. In the Steel Industry, taking the lead in this regard and doing something constructive, is within our power.